Unfortunately, We Do Have to Worry About the National Debt

It brings me no pleasure to say that Dick Cheney was right, until now.

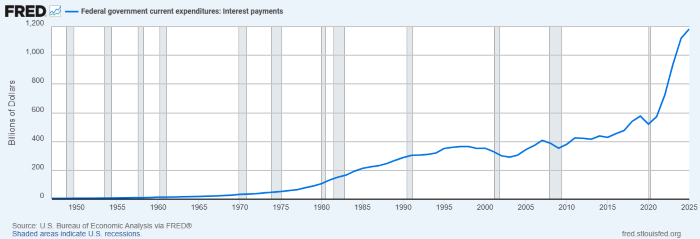

Photo by Reagan White House Photographs Splinter Debt Markets

Republican Vice President slash evil dark lord of the Bush Administration, Dick Cheney, famously said in 2002 that “Reagan proved deficits don’t matter,” and an entire generation of liberals and lefties followed his lead in groaning about the national debt every time someone raised the issue. There was plenty of good reason to, because the Very Serious People in charge of America’s discourse always predictably ask “hOw WiLl YoU pAy FoR iT” every time someone proposes to feed starving American children, but they will never ever ask the same questions of the budget to build bombs that murder children halfway across the world. The Very Serious People who have cited the national debt as reason to oppose any policy to the left of George W. Bush’s administration are predominantly bad faith actors whose every word on every subject can be ignored. Besides, they were wrong and Dick Cheney was right—at the time, at least.

In 2002, the Fed Funds Rate, the rate the Federal Reserve sets in order to try to anchor interest rate expectations in the bond markets, was about 1.75%. The total public debt in 2002 was about $6.2 trillion, and our annual interest payment on the debt was about $301 billion dollars. That is a rounding error for a roughly $11 trillion economy. Interest payments on the debt were not a problem for the U.S. government, until now.

In 2019, we paid about $577 billion in interest on the debt, a record high. That quickly ballooned into a $1.18 trillion bill in 2025. That’s $261 billion more than the U.S. spent on defense last year. The national debt is opaque and complex and some spooky ghost haunting an unknown future, but the interest payments we make on it every year are very real, and they’re called the bond market. That’s your money that comes out of the budget and goes into investors’ pockets (which are largely foreign governments, domestic pension and mutual funds, and the Federal Reserve). This is not some minor footnote anymore, it is the second-largest percentage of the current 2026 budget, tied at 14% with healthcare and Medicare, and 1% ahead of national defense spending under Pete freaking Hegseth and a GOP trifecta.

We occupy a very different world than the one that Dick Cheney and Ronald Reagan inhabited. The FRED chart of annual interest payments on the debt looks like a shitcoin going parabolic before a crypto scammer inevitably rugpulls it. The massive government spending unleashed by the pandemic shock fundamentally changed the global financial world.

Government deficits matter to varying degrees in varying contexts because that’s where interest rates come from, and they affect everything from your mortgage to your credit cards to the cost of products you buy. There’s a very good reason why the Fed’s primary tool to steer the economy is the Fed Funds Rate, and yet again I would like to take this opportunity to call out our vacuous stock market-focused press who only covers one financial market that is dominated by the top 10% of earners while largely ignoring the largest, most liquid market in the world. No one can hide from the U.S. Treasury market, because interest rates are just the price of money, that thing we all need to live. And America has demonstrated in recent years that we are a lot less trustworthy than our debt’s “risk-free” global status might suggest, and last year the dollar had its worst start to a year since 1973.

Starting from the day before Trump won the 2024 election, the U.S. Treasury yield curve has contorted itself into a set of returns that one could call stagflationary. Interest rates on short-term debt–the one, two and three-year Treasuries–are down over 13%, 7.5%, and 5.8%, respectively (on a relative basis). The five-year yield is down 3.1%, while the seven-year is basically flat, down 0.28%. That primarily tells a story about Trump’s unprecedented desire to destroy the Fed’s independence and anoint himself King of Zero Interest Rate Policy (ZIRP), but it also reflects expectations for U.S. economic growth over the next seven years thanks to the lasting impacts of Trumpinomics.

Interest rates going up means more growth expectations (inflation expectations notwithstanding), while interest rates going down means lower growth (ditto). The market is not expecting Trump to be around in seven years, despite what many political doomers taking Trump at his word will tell you. Those returns on U.S. debt are not just about his war on interest rates and the Fed. They are a warning to us about a slowing economy.

But as you get towards the long end of the yield curve–those debts America must repay long after It likely Happens–those interest rates are up. The 10-year Treasury Bond, the most important debt instrument in the world that determines your mortgage rate, is up 2.41% on a relative basis. The 20-year, a relative weird newcomer to the debt party, is up over 8.81%, and the 30-year that pensions and other long-term investors anchor their gargantuan portfolios around, that’s up 11.6% since Trump won the 2024 election. That tells a story of duration risk, when investors decide that there is increased risk that longer term debt may not get repaid when it comes due, so they demand a higher interest rate in order to incentivize them to smash the buy button and loan some money long-term to a bunch of folks who elected Trump twice. This new risk could come in a lot of forms, one being the lower future growth story the short and middle end of the curve has told, which will provide the government with less money to pay down its longer-term debts with.

The U.S. debt to GDP ratio just surpassed 100%, meaning that the $31.9 trillion in debts we owe could not be covered by our $31.4 trillion in annual GDP. Zerohedge-style doomers will yet again say this means that the end is near for the ten trillionth time, but that ignores the fact that Japan has lived decades of this debt-laden life, and they have avoided serious repercussions for this so-called reckless spending—until now, where they find themselves in a much murkier world.

Their debt to GDP is at 235%, a very unnerving figure that is orders of magnitude more harrowing than ours. New conservative Prime Minister Sanae Takichi announced a plan to both cut food taxes and engage in deficit spending, and the bond markets have revolted. The Japanese one-year bond yield is up almost 1,500% on a relative basis since January 2024. The 10-year Japanese bond yield was negative 0.3% in 2019–meaning you paid Japan extra to lend Japan money for a decade–and it is paying you 2.5% interest now. The immediate rates the Bank of Japan paid were sub-zero from 2016 to 2024, and it is now at a 30-year high of 0.73%. That is what an economic regime change looks like, where the math fundamentally changes investors’ calculus.

The Bank of Japan has long been at the bleeding edge of inventive monetary policy and fiat-driven ingenuity, so their story is the opposite of straightforward and easily understandable, but the basic mechanics of how governments finance their budgets mean that ultimately, global investors have the final say in lending costs. No one has to lend any government money if they think there is a better low-to-no risk option out there for giants like central banks, pension funds and insurance pools to park their long-term cash.

That is the story that gold has told ever since Trump won, as many investors have come to evoke a pre-fiat era where the globe’s original financial meme anchored the market’s financial trust. Long-term government bonds in every country have seen their yields spike as investors balked at lower rates, as it is an open question what these major governments all with debt to GDP ratios over 100% will look like in 10, 20 and 30 years. Especially in an aging Europe. So instead of trying to figure out the answer to that long-term unknown, a lot of big players have avoided the headache altogether and just bought gold.

We have left the era of ZIRP borne out of the 2008 crisis, and entered a new world with higher interest rates thanks to the COVID crisis changing the math of money. The supply shock marking the end of an age of excess spiked inflation to 9% in 2022, and short-term interest rates have come down to more manageable levels around 3%, but long-term debt across the world has floated upwards ever since a sobering event that has reminded investors that someday, these cans continually being kicked down the road will become too heavy to move.

No one wants to be left holding the bag when this unsustainable era meets a financial shock it cannot overcome. Past economies thought they had finally figured it out too, then years like 1847 and 1929 and 2008 all imprinted themselves on the culture and reminded us how capitalism definitionally cannot boom without comparable busts.

Takaichi’s example is one that every future liberal politician must take into account, because you cannot just declare that you are going to do more government spending that runs deeper deficits in a debt-laden era and not expect the bond market to react. They will impose higher interest rates on you, which in turn will make these government spending plans more expensive thanks to higher annual interest payments. And no, we can’t just jack taxes all the way up on the wealthy and pay for all of it. We will obviously have to soak the rich in taxes should serious liberals ever take power again, but anyone who has done the back of the envelope budget math for the United States knows that the top 10% alone do not have anywhere near enough to cover decades of financial neglect and generations of hubris.

This is why all the slopulist policies from know-nothings like Cory Booker that call for no taxes on people under a certain income are beyond stupid and undercut any agenda centered around using the government to help people. We don’t have to pay down the debt like all the Very Serious deficit scolds say we do, but we do have to find a way to pay less annual interest on it than we spend on the fucking Pentagon. If you lower taxes, you reduce the government’s income. Governments then have to issue more debt (bonds) in order to cover greater annual deficits, and this increased supply reduces the price of them (and because interest rates move inversely to bond prices, this pushes rates up).

If we are to build a new and more equitable future, everyone—everyone—is going to have to pay higher taxes than they do now.

It sucks to live in a universe where Dick Cheney was right in ways that only benefited Dick Cheney, and now he is wrong in ways that do not benefit us, but that is the world that the last generation of politicians from each party has built for us. They were not good stewards of America, and they ran up major deficits while kicking every can they could find further down the road, all in the name of building an age of anti-democratic elite impunity that is comparable to the Gilded Age that preceded and helped cause the Great Depression. The plan from the Reagan revolution onward was to party like it’s 1999 and make their children and grandchildren pay for it. That is the legacy of the boomer political generation. They left the political world worse off than when they found it.

We are the children of that political generation forced to pay for their excess, and we must find ways to address the debt responsibly, lest the bond market charge us a higher interest rate to build a future that’s more hopeful than the one delivered unto us. We don’t necessarily have to pay down a bunch of debt either, finding a way to lower interest rates is the other part of this equation that can reduce our debt burden (ie: 1% times a trillion is a lot less than 4% times a trillion), and we were on the path to a much more sustainable interest rate future before Trump’s stagflationary economic policies pushed inflation off the downward course it was on since 2022. Austerity economics will always point to the big scary debt number to justify its one idea that has proven not to work, but the Bank of Japan has demonstrated there are lots of ways a country can keep interest rates low amidst rising debt burdens without the shit hitting the fan, for now.

Should Trump plunge the world into crisis when oil stockpiles run dry next month, this will only exacerbate the stagflationary dynamics he has been pumping into the economy over the past year. The Fed has taken rate cuts off the table and has begun to speak about rate hikes due to the inflation the oil shock is certain to bring. The two-year Treasury yield, the one most sensitive to Fed policy, is up nearly double the one-year yield since Trump and Israel’s war on Iran began, 16.4% to 7.6% on a relative basis. It seems very likely that our already gloomy debt picture will be exacerbated by lower growth and fewer government receipts, but with higher inflation and more arduous debt payments alongside it.

The debt problem is a can we can only kick down the road for so long, and given how Republicans only give a shit about it when Democrats are in power, it seems likely that Democrats will have to find a solution to this mounting mathematical problem that is costing all of us more money every year than the Department of Defense. If these trends continue, we all need to get used to much higher interest rates for the rest of our lives.