Economic Sentiment Collapses to All-Time Lows, Why?

A new consumer sentiment survey suggests things are worse than 2008, how is that possible?

Photo by Joe Raedle/Getty Images Splinter Economy

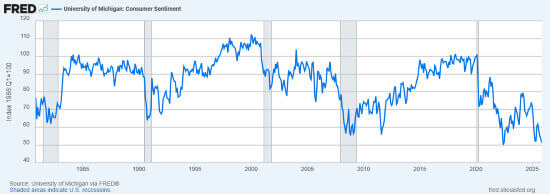

If you only looked at the gold standard(?) Michigan Consumer Sentiment survey’s new report, you would think we were in the midst of a generational economic crash surpassing the scale of the 2008 Great Financial Crisis or the stagflationary malaise of the 1970s where the Misery Index hit all-time highs. A new survey is out today, and it reveals a populace with incredibly negative forward-looking views on the economy. This certainly is related to Trump, who per a recent AP-NORC poll, had his lowest approval rating ever on the economy (31%), which surely helped prompt president sundown to rant to the country on primetime TV this week. But the fact that the 2025 line is digging down as deep as the 2022 line proves that this is not a Trump-centric dynamic, and people feel bad about the economy for reasons that go beyond tariffs and all his other ineffectual bullshit.

Source: University of Michigan via FRED®

Those grey bars indicate recessions, revealing why this is, or perhaps was, looked to as a gold standard for consumer sentiment. By the pattern established over the last half-century, there should be grey bars in 2022 and right now, and yet, GDP is growing. One might think this is because of our age of inequality, where this survey picks up the bulk of people struggling while the economy is held up by the wealthy (a dynamic that is true that I will dig into in the K-shaped recovery section), but the truth is that wage growth for the lowest earners has grown relative to higher earners since the pandemic. As Matt Darling demonstrates by parsing out the consumer sentiment data, a lot of this new negative sentiment is actually coming from the top income tercile, revealing the backlash from capital against labor in response to the strong labor market we experienced in the wake of the pandemic shock. There is not one singular explanation for what is happening to the economic vibes in America.

University of Michigan Consumer Sentiment index

— Matt Darling (@besttrousers.bsky.social) December 18, 2025 at 6:17 AM

This has become an exhausting debate because a lot of people who lack economic expertise are certain that either non-economists like Will Stancil are right and everyone has gone completely insane, or those dogpiling him in his mentions claiming that the GDP figures are lies and we actually have been in a Great Depression for a few years are certain they’re right. If you pay attention to the actual trained economic knowers, certainty is not a feature of their analysis. That has been beaten out of every one of us to step into a serious financial arena. You know nothing. You are nothing. The whole world is a range of probabilities, and you will be humbled by it. All we can say for certain is that after the pandemic, the vibes drastically changed for a lot of Americans, and you can see it in the split between the Conference Board’s Consumer Confidence survey and the University of Michigan’s.

🚨USE THE CONFERENCE BOARD MEASURE OF CONSUMER CONFIDENCE! IGNORE MICHIGAN–DO NOT RUN AWAY WITH GRANDIOSE INTERPRETATIONS OF THE WORLD BASED ON UMICH!🚨

— Julia Coronado (@jc-econ.bsky.social) December 19, 2025 at 9:22 AM

Their methodologies are different, which certainly gives us some insight into the post-2020 divergence. The Conference Board asks respondents about current business and employment conditions as well as business conditions, employment, and income expectations six months from now, while UMich asks people about their personal finances, buying conditions and future expectations for the economy. It’s clear now that for economic forecasters, survey questions about personal finances are not useful to understanding a broader economy chugging along fairly well in large part thanks to gargantuan AI capital expenditure spending. That the United States has grown out of the pandemic far faster than its peers is also lost in all the bad vibes.

But something is clearly going on that’s deeper than ‘people let TikTok make them think they’re destitute’ or ‘economic data is bourgeois bullshit,’ and I will venture some guesses here as to what is happening. Because despite all the online squabbling that has taken place around the vibecession since 2022, there is something real and important to all this. Consumer sentiment roughly translates to consumer spending, the engine of our economy (at least before AI), hence why recessions coincide with collapses in it. This is serious stuff, and it can’t all be handwaved away as vibes.

The K-Shaped Recovery

This is a title of a 2021 paper from the Bureau of Labor Statistics (BLS), and you don’t need an economics degree to understand the point it makes, just look at the shape of the letter K. One diagonal line is going up, and the other is going down, resembling the most important chart in American politics and economics over the last fifty years.

Americans don’t get paid well relative to the productivity we create. Capitalism is built by capital, and so the spoils of it go to them. This has been true for decades, as the above chart demonstrates, so this cynicism is clearly not solely responsible for the recent drop in consumer sentiment, but I do think this raw deal has become more salient since the pandemic. I screenshotted these charts from the BLS report which tracked percentage changes in employment from February 2020 to May 2021, broken down by five income buckets, and a clear pattern emerges. Pay attention to the orange lines tracking employment loss due to closures. People at different income levels live in different worlds.

Digging into the vibecession stuff again today and I think these charts from a 2021 BLS paper on the K-shaped recovery are instructive. www.bls.gov/osmr/researc…

— Jacob Weindling (@jakeweindling.bsky.social) December 19, 2025 at 10:22 AM

As I detailed in my piece about the poverty line last month, it’s a lot higher than our mainstream discourse thinks. It’s not $140,000 per year like one viral economic blogger suggested, but a much more thoughtful measure called Asset Limited, Income Constrained, Employed households (ALICE) finds that 42% of American households—55 million—fall below their financial hardship threshold. It is adjusted for cost of living by county, and this gets to the heart of the alleged K-shaped recovery that admittedly has become a bit messier of a narrative as time has gone on and lower income wages have grown, although the core structure of the letter remains in place as a broader economic principle.

“If there’s a single stat to capture what’s happening to the economy, it’s this: The top 10% of U.S. earners now make up half of all spending, and it’s changing everything,” wrote journalist Matt Pearce today. “Delta Air Lines expects to make more money soon from luxury and business fliers at the front of the plane than from everybody else.”

I wrote about this revelation from Moody’s Analytics earlier this year, and how connected it is to the stock market creating a wealth effect fueling this spending. “Affluent people also found themselves with assets, such as stocks, that suddenly were worth far more,” wrote the Wall Street Journal back in February. “The net worth of the top 20% of earners has risen by more than $35 trillion, or 45%, since the end of 2019, according to Federal Reserve data. Net worth grew at a similar rate for everyone else, but it translated to a lot less money: an increase of $14 trillion for the bottom 80%.”

Many Stancilites will point to the fact that wage growth for the lowest earners has outpaced those of higher earners, but fail to recognize the facts of a rate of change metric. Look at those charts I screenshotted above, measuring from 2020 is measuring from a complete collapse, and while ten steps back and seven steps forward does give you a pretty good rate of change result, you’re still down a net of three steps from where you started. That’s the employment situation a lot of low wage earners are dealing with these days in our cooling job market, and jobs like cashiers that once were some of the most prevalent in America are now being replaced by robots. The same is true for entry level college graduates, as the bottom layer of many organizational charts is being replaced with AI as we speak. That may help the company save money and aid executives’ spending fueled by their stock-based compensation that makes topline economic figures look good, but it doesn’t do much for the low wage worker whose job is being replaced and isn’t seeing the benefits of the broader economy. In many ways, AI is the poster child for the K-shaped economy. Executives like Elon Musk are openly plotting to kill our jobs, and are promising us a future utopia with “universal high income” at an undetermined later date.

Inflation is higher for the bottom leg of the K too. Inflation hits lower earners harder for the simple fact that one divided by fifty is a higher percentage than one divided by fifty thousand, and while overall inflation has been coming down since its peak in 2022 coinciding with the low in the consumer confidence survey, specific goods that lower income people spend the majority of their money on have not dropped as far as topline inflation has.

The latest inflation figures felt a bit soft and could be due to just wonkish changes in methodology, but rigging BLS numbers is very difficult and until there’s real evidence of it, no one should think that Trump’s tentacles have reached this far yet. Taking the latest inflation print at face value, the topline figure of 2.7% inflation is good. The Fed’s target of healthy inflation is 2%, so it stands to reason that things should feel like they’re stabilizing, right?

Except that food away from home at restaurants is at 3.7% year-over-year inflation. Meats, poultry, fish and eggs are 4.7%, shelter is at 3%, medical care services is at 2.9%, used cars and trucks is at 3.6%, while energy, a big monthly percentage cost for middle class and lower income earners, is up 4.2%, with natural gas up a stunning 9.1%. Energy prices are rising for a lot of reasons, AI data center demand, tariffs, Trump destroying a revolution in clean energy and domestic manufacturing and restricting the supply we can deliver to our energy grid, and a lot of geopolitical stuff that would turn this into a 10,000-word blog, but the net result is that everyone’s paying a noticeably higher energy bill this winter than they were last winter. Trump points to the price of oil being low which is true, gasoline inflation is just 0.9%, but in a work-from-home world willing to buy Nazi cars if they’re electric, that matters less than how you power your home and business, which is not with gasoline.

Ever since the pandemic, the stock market has shot off to all-time highs, taking the net worths of stock holders to all-time highs. Between their spending and seven companies creating a human centipede of centibillion-dollar AI investments, that is basically what is powering the bulk of the economy. That is why the vibes are shit. Because people go to the grocery store and can’t afford steak anymore and then are told that they’re just hallucinating their own economic misery as they scroll their phone and see Mark Zuckerberg shrugging his shoulders over potentially setting $500 billion on fire. Our modern Gilded Age has created siloed economic worlds whose lived experience is very different from each other depending on how much you make, how many assets you own and where you live. If it feels like different economic classes of Americans inhabit different economic realities, that’s because they do.

Anchoring to 2019

But we do have to give the vibes caucus some credit here. It’s not called the vibecession for nothing, and we would be a lot better off if the explanations of the term’s inventor, Kyla Scanlon, were more central to the online discourse than the former political candidate whose opponents mailed his own posts to his constituents as an attack ad. This is nuanced stuff, and each side of the vibes vs. recession argument has a point, as Scanlon wrote in December 2023, “A slowdown in the rate of increase in price levels doesn’t really mean all that much when you’ve been living in an absolute price pressure cooker for three years.”

Some prices are lower than they were in 2022, but higher than they were in 2019, and they’re not the only drastic shift the entire populace has experienced. Computer work for many above a certain income level has fundamentally changed, while those working in brick-and-mortar businesses and manufacturing cannot afford the same luxury. Many people are still dealing with the physical health and economic problems imposed upon society by a global pandemic that still has not ended, while social media is an even more ubiquitous force in our lives. We are just aware of more anecdotal stories of struggle now, which has made it more difficult to see the bigger economic picture amidst the worst inequality in a century. Add in the actual precarity around 42% of households feel per ALICE’s data, and this is a perfect cocktail for confusion.

But the root of it is that the world changed and our expectations for it largely have not. The 2024 election was many things, but pressing a button to return to 2019 was absolutely behind a lot of people’s shockingly naive Trump votes. Something fundamentally broke in our society in 2020, a kind of trust that underwrites civil societies across time, and it manifests itself in every realm, especially economics where the split between the haves and have nots is most measurable. People feel bad about their situation relative to before the whole world changed seemingly overnight, and they are more aware of those who are benefiting from this period of collective misery. People know that The Great Gatsby is taking place every day in every major American city, and we can only hope that these people will not deliver us a future like The Grapes of Wrath.

Anchoring is a very important financial concept. One of the things that surprised me in my finance classes was how central psychology was to many of them. The expectations that you set for yourself are of utmost importance because they serve as an anchor, and how you perceive everything else becomes relative to those expectations. In the wake of the 2008 Great Financial Crisis, Americans experienced unprecedented levels of cheap credit that fueled a generation of affordable burrito taxis and other creature comforts of consumerism. When investors could weaponize Zero Interest Rate Policy (ZIRP) to load up on low-to-no-interest debt and then use that debt to invest in companies whose future cash flows became inflated thanks to ZIRP math, consumers had it easy as countless cans got kicked down the road. Tech giants arming themselves for their societal takeover in this era were and are able to carry immense debt levels because it cost them nothing to do so, and the simple change of a zero to a two, three, four or even nine back in 2022 has fundamentally altered the entire economy to a mathematical degree that many people just can’t understand, including the president, who is practically demanding that the next Fed governor bring ZIRP back as a requirement to get the job.

Our expectations are still anchored to a world built by ZIRP. A world of easy money delivering us cheap burrito taxis and fueling the economy in the wake of a gargantuan economic collapse. A world where Elon Musk can become the richest man alive by creating the greatest meme stock in history, entirely fueled by the easiest money in a generation, enabling you to get rich off stupid speculative bullshit too. A world where Donald Trump could build a path to the presidency on cheap credit after going bankrupt six times. A world where cryptobillionaires buying their own libertarian islands is a real thing and not some modern James Bond plot. One of the many indignities of the K-shaped recovery out of 2020 is that we did get ZIRP again in that crisis, but it only benefited asset holders and created an excessive speculative mania, while it delivered consumers 9% inflation.

The world of cheap burrito taxis is gone, and a lot of the deteriorating vibes are centered around the cost that higher interest rates and better wages for low wage workers have imposed on products that were cheap and accessible a decade ago. Trump is the avatar for the broad-based misunderstanding of this post-ZIRP era, where he is determined to make the same mistakes as the stagflationary 1970s in a desperate bid to make ZIRP great again and bring its creature comforts back.

The Great Financial Crisis

Perhaps it is because I graduated into the job market in 2009, a year where we began losing 800,000 jobs a month, and thus have a bias about 2008, but I think it is the central fault line in our present age. It is where both the capitalist backlash on the left and the reactionary fascism on the right have sprung from, and where fervent modern distrust of the establishment was born. The Iraq War was our generation’s Vietnam, but the widespread age of distrust began when a bunch of criminals defrauded the world and came within days of completely nuking the entire global economy. The Troubled Asset Relief Program (TARP) is wrongly looked back at negatively for many reasons—a lot of leftists falsely attribute the bailout to Obama, but a simple recap of the nature of linear time will reveal this was a Bush bailout—and it is reviled by many for being a handout, but that is wrong too. We got paid back. The best critique of TARP was that it wasn’t big enough and Congress chickened out because they didn’t want to vote for something with a trillion-dollar price tag even though the scale of the crisis could only be measured in the trillions.

A gigantic hole got blown in the economy by fraudulent financial schemes orchestrated by the uber-elite, upending millions if not billions of people’s lives for a generation. We know that those like me who graduated in its wake have had their professional prospects harmed relative to people who did not graduate into the genesis of ZIRP, while professions like lawyers and academics suffered, and the economy changed in a very fundamental way. The bitterness around TARP is that in 2008, Wall Street got bailed out but Main Street didn’t, which is a valid criticism, but Wall Street had to get bailed out. We had no choice; we’d be using bottle caps for currency right now if we hadn’t.

But instead of fixing the fundamental economic problems in our age of inequality revealed by 2008, we just flooded the zone with cheap debt which jacked up asset prices and made inequality exponentially worse. What once was viewed as a policy only to be utilized in emergencies now became a decade-plus of a wildly distorted and anomalous status quo. We didn’t fix what 2008 broke, we just built a land of unsustainable burrito taxis and increasing financialization hacking the magic of zero percent interest rates. When 2020 rolled around and we were forced to enact emergency ZIRP measures again, this didn’t spawn another wave of affordable burrito taxis, but dog coins and inflation, proving the limits of this policy.

I wrote last week about why gambling is everywhere, because the scam economy can be accessed by anyone now, and as dismaying as the rise of prediction markets and sports betting and crypto and zero date options trading and all other forms of high-risk gambling spreading to every nook and cranny of the world has been, it’s just following the broader trend in our hollowed-out and speculative economy. You don’t make it in a capitalist economy by selling your labor, that’s the sucker’s way out. You make it in a capitalist economy by buying assets, and that fact has become evident amidst 42% of households struggling to build wealth in the face of all-time high house prices and an all-time high stock market. I think consumer sentiment is near all-time lows because of a combination of real and widespread economic hardship, the drumbeat of the vibecession narrative on social media and major media reinforcing anecdotal evidence of real hardship, and the gobsmackingly shameless greed of the wealthy. It has all led many people to agree with George Carlin’s most famous line: it’s called the American Dream because you have to be asleep to believe it.