Squid Game Relishes the Bleak Fatalism of Debt

Squid Game is billed as "dystopian," but its resonance is universal

EntertainmentTV

Spoilers for Squid Game ahead.

The question of how far some people would go to free themselves of debt is at the heart of Squid Game, a breakthrough hit for Netflix that is poised to be the platform’s most popular show in its history. Directed by Hwang Dong-hyuk, the South Korean import is a diabolical, original parable about money and debt—specifically, what the average person is willing to sacrifice in order to earn enough to live a life free from financial obligations—and is, unsurprisingly, resonating with viewers globally.

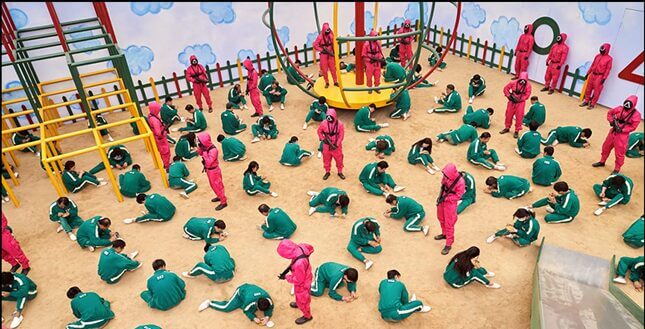

Squid Game is a broad critique of capitalism, but it’s largely about how hopelessness in the face of debt translates to real-life decisions and actions. In the show, hundreds of people crippled by personal debt make the decision to participate in a series of childhood games in exchange for a cash prize—$45.6 billion won or roughly $38 million dollars—which accumulates in a glowing gold orb suspended over the contestant’s shared barracks, the metaphorical carrot dangling in front of their eyes. The rules are simple: Play the games to advance to the next round. If you lose, you die, executed by a sniper or at close range by a team of silent masked Managers, dressed in pink jumpsuits, executing orders like Stormtroopers.

At the center of the game is Seong Gi-Hun (Lee Jung-jae), a divorced man saddled with gambling debt who is struggling to pay back his loan sharks to maintain a relationship with his daughter and provide for his ailing mother. Along with 455 other people desperate enough to risk their lives for the chance at financial solvency, Gi-Hun joins a motley cast of characters, all with different motivations: Cho Sang-Woo (Park Hae-soo), Gi-Hun’s childhood friend, has a successful career but is wanted by the police for stealing money from his clients; Kang Sae-byeok (Jung Ho-yeon) is a North Korean defector who needs the money to extract the rest of her family; Abdul Ali (Anupam Tripathi) is a Pakistani immigrant who needs the money to support his family because he hasn’t been paid in months; and Oh Il-Nam (O Yeong-su) is an elderly man with a brain tumor who is in the game only because waiting for death inside its walls is preferable to doing so in the real world.

As one of the masked managers says over the duration of the show’s nine episodes, the gameplay is essentially the platonic ideal of a meritocracy; by stripping everyone of their social status and putting them on equal footing, they all have the same chance of success. But the situations that the players find themselves in are much like life, in that luck, physical strength, knowledge, and the myriad other uncontrollable elements factor in their success. Equality is a myth that the game itself purports to uphold, but in the first minutes of the first game—the childhood favorite Red Light, Green Light, where losing contestants are shot by snipers— it becomes clear how this will all go down.

The trick of the game is that there is no freedom, after all—or at the very least, freedom comes at a cost. Squid Game’s contestants have accepted this fatalism into their hearts, because climbing out of their debt otherwise is inconceivable. Debt, in this case, is fatal.

In that way, Squid Game is less dystopian than it might seem. Writing for the Associated Press, Kim Tong-Hyung notes that the crippling debt experienced by the fictional contestants of the show is similar to that of many South Koreans right now:

Many South Koreans despair of advancing in a society where good jobs are increasingly scarce and housing prices have skyrocketed, enticing many to borrow heavily to gamble on risky financial investments or cryptocurrencies.

Household debt, at over 1,800 trillion ($1.5 trillion), now exceeds the country’s annual economic output. Tough times have pushed a record-low birth rate lower as struggling couples avoid having babies.

Squid Game’s resonance is universal, even though the likelihood of the game itself happening in real life is slim. Desperation is commonplace, a part of life that those with debt compartmentalize daily. As it currently stands, my student loan debt hovers around the $20,000 mark—not a lot by most standards, but not an insignificant amount of money either. For a time in my 20s, I was very bad with money, deferring my payments a few times during stretches of hardship and once, almost defaulting on my loans. After spending a fair amount of my 30s rebuilding my credit and figuring out how to manage my money, I dutifully restarted paying my debt down in earnest. The debt is merely a part of my existence now, another line item on the list of bills I pay every month.

At varying points in the 17 years since I graduated college, I have felt its crushing weight. For a time, I entertained the fantasy of faking my own death, completely absolving myself of financial obligations by pretending to disappear. Though this would’ve solved my problems temporarily, the fact is the debt I owe would transfer to my father, so freeing myself from my problem would’ve been just an easy way to pass the buck. What makes debt so overbearing is not merely the number, but the concept itself. Sometimes people must take desperate measures.

My debt is still there and will be there in some fashion for the rest of my life. My relationship to this inevitability was formed in childhood; I grew up with an intimate understanding of my small family’s finances, overhearing conversations about between my divorced parents about my mother’s Macy’s card and moving frequently between rental homes as my father, a former academic, took whatever jobs he could in order to support us. When my father bought our house, he did so using the small amount of money left to him by my grandmother after she died; home ownership was never really in the cards, because adding yet another gargantuan bill to the pile was inconceivable. Instead of attending college after high school, I was forced to take a year off, because the financial aid package I received was a mere pittance. We didn’t have the money to cover the balance, and the thought of taking on the massive amount of debt that would’ve enabled me to attend was too much to bear. (Though I started college a year later, with a slightly more robust aid package, it still wasn’t enough. I feel certain that I will be paying this off until I die.)

My story is not particularly unique. The cry to cancel student loan debt across the country rages on, as progressive lawmakers are currently urging President Biden to use his executive power to eliminate student loan debt across the board. A life lived under the shadow of debt’s great mass is essentially a version of Squid Games without the distraction of childhood games—just an endless pressure and sense of obligation that hangs over every decision you make with your money. So many of us live with this weight as a matter of course, because there is no other option—life plods ahead in spite of these obligations, and we are all making do under a system that benefits very few.

Just like the revolving door of debt, Squid Games sets up its contestants for failure, knowing full well that the chance of survival is based on an unforeseen set of circumstances that is out of their control. But the human urge to support one another despite operating within a system that is unsparing in its cruelty prevails. Living within the shadow of financial ruin is a difficult pill to swallow when you know that your obligations to pay back what you owe are to a faceless entity that cares little about your humanity. The power to make debt disappear is concentrated in the hands of the very powerful, and everyone else living under its oppressive thumb is merely at the mercy of their decisions, made out of necessity or desperation, but ultimately for survival.